The Chinese chemicals industry has entered a phase of lower but still solid growth, with chemicals demand growth rates still above global average.

- Slower, but still solid growth

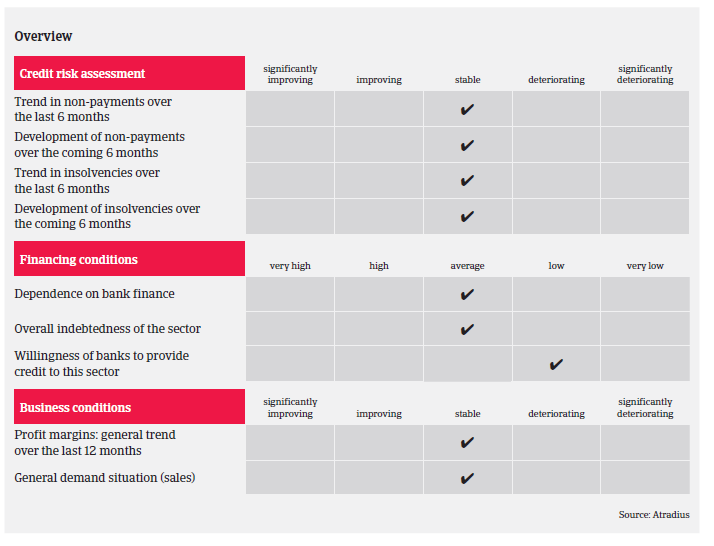

- Payments take around 60-90 days on average

- Private businesses face financing issues

The Chinese chemicals industry has entered a phase of lower but still solid growth, following the slowdown in GDP growth (forecast to increase 6.7% in 2017 and 6.1% in 2018). However, despite the slowdown, both Chinese GDP expansion and chemicals demand growth rates remain above global average.

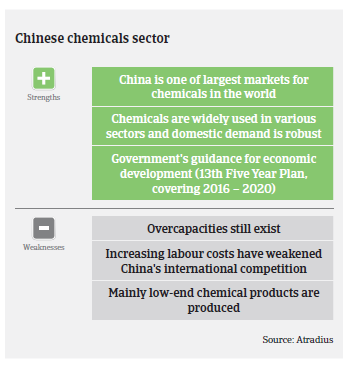

The performance of the Chinese chemicals industry is still hampered by a lack of advanced technology, despite government efforts to accelerate the acquisition of Western know-how. Still many Chinese firms do not invest enough in research and development and rely primarily on imported technology. The government is actively encouraging joint ventures between foreign companies and state-owned enterprises. The benefits for foreign companies investing in China include a growing domestic market in which they can sell their products, and low construction and labour costs when building greenfield projects. In the long term, China’s growing industrialisation and urbanisation will provide further growth opportunities for the chemicals industry, and an expanding middle class will require higher-quality chemical products.

Many subsectors have faced oversupplies because of the investment-led growth model that has resulted in excessive spending on new factories in the past. Overcapacity issues have resulted in deteriorating business profitability in some segments like Purified Terephthalic Acid (PTA) and fertilizers, while the lower oil price has hit the oil exploration industry. However, the oil-refining and petrochemicals sectors recorded sustained growth thanks to cost reduction and robust demand. The Chinese petrochemicals industry achieved revenues of CNY 13.29 trillion (EUR 1.79 trillion) in 2016, and profits remained stable around CNY 644.4 billion (EUR 87 billion) with profitability of 4.8%, on average. Overcapacities have meanwhile abated in the fine and specialty chemicals segment, leading to market stabilization.

Competition in the Chinese chemicals sector is high as overcapacities have driven businesses to reduce output and cut prices in order to gain a competitive edge. This goes at the expense of smaller and medium-sized companies, which have to leave the market or are being taken over by larger entities.

On average, payments in the Chinese chemicals sector take around 60-90 days. The level of payment delays and insolvencies is average in the Chinese chemicals sector, and no major increase of business failures is expected in 2017, as demand for chemical products is relatively stable across all subsectors and among all consumer segments.

Our underwriting approach to the Chinese chemicals sector is generally neutral for all main subsectors (basic chemicals, petrochemicals, fine and specialty chemicals). We take into consideration the performance of each subsector, the background of the businesses’ shareholders, the nature of the buyer (seller or manufacturer), their financial performance and funding facilities. We are more cautious with highly geared private businesses in the chemicals sector, as banks are currently restrictive in offering loans to privately-owned companies, which could lead to serious working capital issues.

Related documents

730KB PDF